In a significant and compassionate ruling, the Income Tax Appellate Tribunal (ITAT), Ahmedabad Bench, has condoned a delay of 153 days in filing an appeal by a senior citizen taxpayer, recognizing her lack of familiarity with tax procedures and digital compliance systems. The decision reinforces the principle that procedural delays should not defeat substantive justice, especially when reasonable cause is demonstrated.

Background of the Case

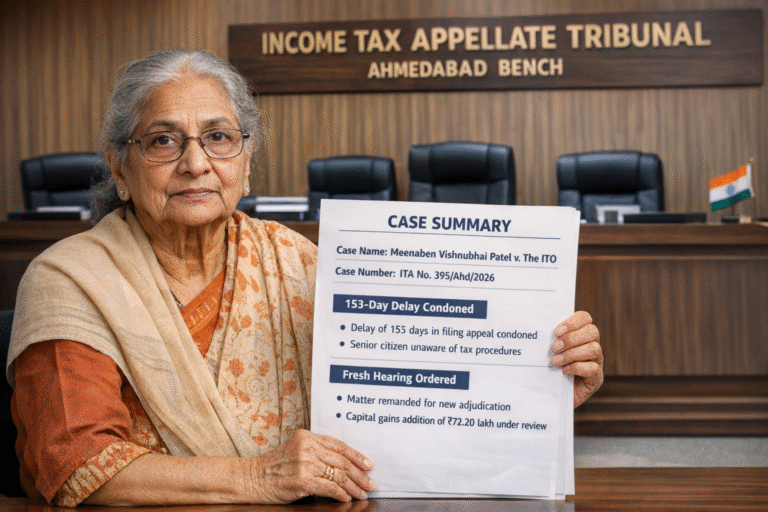

The case, titled Meenaben Vishnubhai Patel v. ITO (ITA No. 395/Ahd/2026), was decided on 23 March 2026 by a Bench comprising Judicial Member Suchitra Kamble and Accountant Member Annapurna Gupta. The appeal arose from an order passed by the Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (CIT(A), NFAC), which had dismissed the taxpayer’s appeal on the ground of delay, treating it as non-maintainable.

The taxpayer, a lady senior citizen, had not filed her return of income and claimed to be completely unaware of the assessment proceedings initiated against her. According to her submissions, she came to know about the ex-parte assessment order only at a later stage. Upon gaining knowledge, she promptly approached a tax consultant and filed an appeal, albeit with a delay of 153 days.

Tribunal’s Observations on Delay

The ITAT took a lenient and pragmatic view of the situation. It noted that the taxpayer was a senior citizen with no prior exposure to income tax procedures or technological systems used in faceless assessments and appeals. The Tribunal observed that such circumstances warranted a liberal interpretation of “sufficient cause” under the law.

In its order, the Bench remarked that the explanation provided by the assessee could not be dismissed as false or untrue. It emphasized that her lack of awareness regarding income tax technicalities and digital compliance frameworks was a genuine constraint. Importantly, the Tribunal held that no negligence or deliberate inaction could be attributed to her.

The ruling highlights a broader judicial approach that prioritizes access to justice over rigid adherence to procedural timelines, particularly in cases involving vulnerable or less-informed taxpayers.

Issue on Merits: Capital Gains Addition

Apart from the delay, the case also involved a substantial addition of ₹72.20 lakh made by the Assessing Officer on account of alleged capital gains arising from the sale of immovable property. The tax authorities had treated the assessee as having a one-fifth share in the property and accordingly taxed the presumed gains.

However, the taxpayer contested this addition, arguing that she was merely a confirming party to the transaction and had not received any consideration from the sale. She maintained that she had no beneficial ownership or financial interest in the property and, therefore, no capital gains could be attributed to her.

The Tribunal found merit in this contention at a prima facie level. While it did not adjudicate the issue conclusively, it acknowledged that the taxpayer had raised a plausible argument requiring proper examination. This further strengthened the case for granting her an opportunity to present her case fully before the authorities.

Restoration for Fresh Adjudication

Taking into account both the reasonable cause for delay and the arguable merits of the case, the ITAT decided to condone the delay and restore the matter for fresh adjudication. The case was remanded back to the Assessing Officer with directions to provide the assessee a fair and adequate opportunity of being heard.

This direction ensures that the principles of natural justice are upheld and that the taxpayer is not denied a fair hearing due to procedural lapses beyond her control.

Key Takeaways

This ruling serves as an important precedent, particularly for senior citizens and individuals unfamiliar with tax compliance systems:

- Liberal Interpretation of “Sufficient Cause”: Courts and tribunals may adopt a lenient approach in condoning delays where genuine hardship or lack of awareness is demonstrated.

- Digital Divide Consideration: The increasing reliance on faceless and technology-driven tax systems must account for taxpayers who may not be technologically adept.

- Substance Over Procedure: Procedural delays should not override substantive rights, especially when the taxpayer has a credible case on merits.

- Opportunity of Hearing: The ruling reinforces the importance of granting taxpayers a fair chance to present their case before any adverse decision is finalized.

Conclusion

The Ahmedabad ITAT’s decision in Meenaben Vishnubhai Patel v. ITO is a welcome step towards ensuring equitable tax administration. By recognizing the practical challenges faced by senior citizens in navigating complex tax systems, the Tribunal has reaffirmed the human element in judicial decision-making. The ruling strikes a balance between procedural discipline and substantive justice, sending a clear message that genuine hardships deserve consideration within the framework of law.