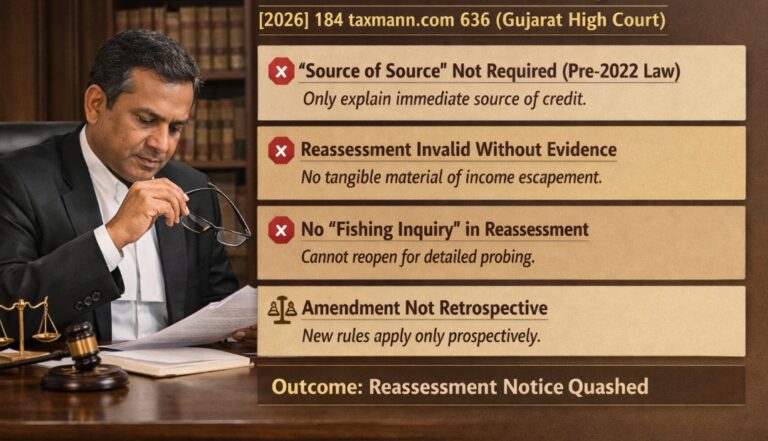

In a significant ruling reported in [2026] 184 taxmann.com 636 (Gujarat), the Gujarat High Court has once again reinforced the legal boundaries governing reassessment proceedings under the Income Tax Act. The Court quashed a reassessment notice issued by the Assessing Officer (AO), holding that for assessment years prior to the recent legislative amendments, an assessee is not required to explain the “source of source” of funds. The judgment also emphasized that reassessment cannot be initiated without establishing actual escapement of income based on tangible material.

Background of the Case

The case revolved around the reopening of an assessment under Sections 147 and 148 of the Income Tax Act. The assessee had received certain credits in its books, such as share capital, unsecured loans, or similar financial transactions. During the original assessment proceedings, the assessee had duly furnished necessary details to substantiate these credits. This included documentation to establish the identity of the creditors, the genuineness of the transactions, and the creditworthiness of the parties involved.

Despite this, the AO later issued a reassessment notice alleging that the assessee had failed to adequately explain the “source of source” of the funds. In other words, the AO sought to question not just the immediate creditor, but also the origin of funds in the hands of such creditor. This formed the basis for reopening the assessment.

Key Issue Before the Court

The primary issue before the Gujarat High Court was whether, for pre-amendment assessment years, the assessee could be required to explain the “source of source” under Section 68. Additionally, the Court examined whether the reassessment notice was valid in the absence of concrete evidence suggesting escapement of income.

Court’s Observations and Ruling

The Gujarat High Court ruled in favour of the assessee and quashed the reassessment notice. The judgment is noteworthy for several reasons.

Firstly, the Court categorically held that for assessment years prior to the amendments introduced by the Finance Act, 2022, the law did not mandate an assessee to explain the “source of source.” The requirement under Section 68 was limited to proving three essential elements: the identity of the creditor, the genuineness of the transaction, and the creditworthiness of the creditor. Once these conditions were satisfied, the burden on the assessee stood discharged.

The Court clarified that the expanded scope requiring verification of the “source of source” is a result of subsequent legislative amendments and cannot be applied retrospectively. Therefore, any attempt by the AO to impose such an obligation for earlier years would be contrary to law.

Secondly, the Court found that the reassessment proceedings were initiated without any tangible material indicating escapement of income. It reiterated the well-settled principle that reopening of assessment must be based on a “reason to believe” and not merely a “reason to suspect.” The AO must demonstrate a live nexus between the material available and the formation of belief that income has escaped assessment.

In the present case, the Court observed that the AO had failed to bring on record any new or fresh information that could justify reopening the assessment. The reassessment appeared to be driven by a desire to conduct further inquiry rather than by evidence of income escaping taxation.

No Scope for Fishing Inquiries

Another important aspect of the ruling is the Court’s strong disapproval of “fishing inquiries” under the guise of reassessment. The AO cannot reopen a completed assessment merely to conduct deeper scrutiny or verification. Such an approach would defeat the purpose of finality in tax proceedings and lead to unnecessary harassment of taxpayers.

The Court emphasized that reassessment is not a tool for roving or exploratory investigations. It is a serious power that must be exercised with caution and only in cases where there is credible material suggesting escapement of income.

Practical Implications

This ruling has significant implications for taxpayers as well as tax professionals. For cases relating to pre-amendment years, the judgment provides strong support against demands for explaining the “source of source.” Taxpayers can rely on this precedent to challenge additions made under Section 68 where the primary burden has already been discharged.

Further, the judgment serves as a powerful safeguard against arbitrary reassessment notices. It reinforces the requirement for the AO to base reopening on concrete evidence rather than suspicion or conjecture.

For tax practitioners, this decision is particularly useful while drafting objections to reassessment notices, filing writ petitions before High Courts, or making submissions before appellate authorities such as the Commissioner (Appeals) or the Income Tax Appellate Tribunal.

Conclusion

The Gujarat High Court’s ruling in this case strengthens the legal position of taxpayers by reiterating two fundamental principles: first, that the obligation to explain the “source of source” does not apply to pre-amendment years; and second, that reassessment proceedings must be backed by tangible material indicating actual escapement of income.

By quashing the reassessment notice, the Court has sent a clear message against mechanical and unjustified reopening of assessments. The decision upholds the principles of fairness, certainty, and rule of law in tax administration, making it a valuable precedent in reassessment jurisprudence.