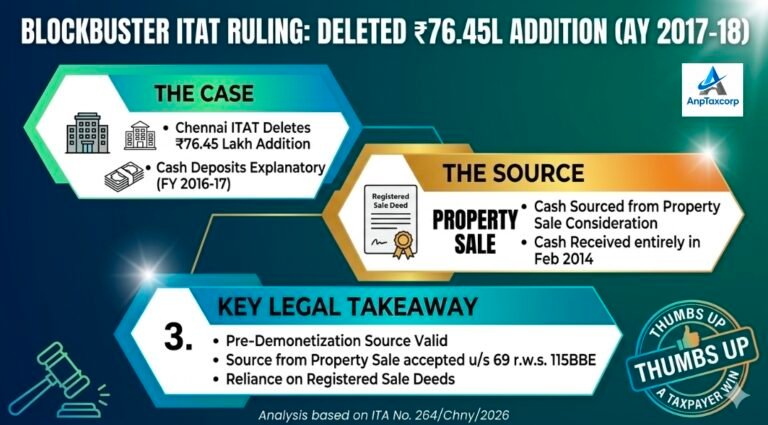

ITAT Chennai Deletes ₹76.45 Lakh Addition on Cash Deposits Sourced from Property Sale

ITAT Chennai has deleted a ₹76.45 lakh addition made under Section 69 read with Section 115BBE of the Income-tax Act, holding that cash deposits cannot be treated as unexplained merely because there was a substantial time gap between the original …