In a significant ruling, the Gauhati High Court has reaffirmed the importance of procedural compliance under the GST regime. The Court held that a Summary of Show Cause Notice (SCN) in Form GST DRC-01 cannot replace a proper SCN as mandated under Section 73(1) of the CGST Act. This judgment underscores the critical role of due process, proper authentication, and adherence to principles of natural justice in tax proceedings.

Facts of the Case

The dispute arose in the case of Garg Associates vs State of Assam & Ors., wherein the petitioner was issued a summary of show cause notice in Form GST DRC-01 for the tax period July 2017 to March 2018. The notice alleged tax liability under Section 73 of the CGST/SGST Act.

Along with the summary, the department attached a document titled “determination of tax,” which it claimed to be the actual show cause notice. However, the petitioner contended that no proper SCN under Section 73(1) was ever served.

Due to the absence of a valid SCN, the petitioner did not file any reply. Subsequently, the department passed an order in Form GST DRC-07, citing non-payment of dues within the prescribed 30-day period.

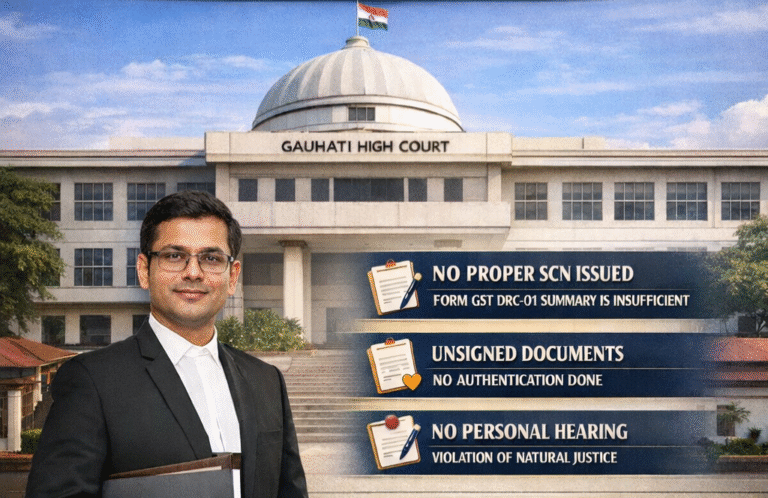

The petitioner challenged the proceedings on multiple grounds:

- No valid SCN was issued

- The attached document was not legally compliant

- Both the notice and order lacked authentication (no signature)

- No opportunity for personal hearing was granted

Interestingly, the department admitted that no separate SCN was issued apart from the attachment. It argued, however, that uploading documents on the GST portal amounted to valid authentication.

Key Issues Before the Court

The Court examined the following critical issues:

- Whether a valid Show Cause Notice under Section 73(1) was issued prior to passing the order

- Whether a summary in Form GST DRC-01 can substitute a proper SCN

- Whether absence of authentication renders the notice and order invalid

- Whether denial of personal hearing violates principles of natural justice

Court’s Observations and Ruling

1. Mandatory Requirement of Proper SCN

The Court categorically held that issuance of a proper Show Cause Notice under Section 73(1) is mandatory. It clarified that Form GST DRC-01 is merely a summary and cannot replace the statutory requirement of a detailed SCN.

The attached “determination of tax” document also failed to meet legal standards. The Court emphasized that the law clearly distinguishes between:

- A show cause notice, and

- A statement of tax determination

Thus, proceedings initiated without a valid SCN were held to be legally unsustainable and in violation of Section 73 read with Rule 142(1)(a) of the CGST Rules.

2. Importance of Authentication

On the issue of unsigned documents, the Court made a crucial observation:

Statutory notices and orders must be properly authenticated by the Proper Officer.

Since no specific authentication mechanism is prescribed under the demand and recovery provisions, the Court applied Rule 26(3), which mandates digital signature or e-signature.

The Court rejected the department’s argument that portal uploading alone suffices. It held that:

- Unsigned documents lack legal sanctity

- Such notices and orders are unenforceable in law

3. Violation of Natural Justice

The Court also addressed the issue of personal hearing under Section 75(4). It held that:

Grant of personal hearing is mandatory whenever an adverse decision is contemplated, irrespective of whether the taxpayer requests it.

In this case, the hearing column was left blank, and the order was passed without giving the petitioner an opportunity to be heard. The Court ruled that this approach:

- Defeats the purpose of statutory safeguards

- Violates principles of natural justice

Final Outcome

Considering these serious procedural lapses, the Gauhati High Court set aside the impugned order. The ruling reinforces that procedural compliance is not a mere formality but a substantive requirement in tax law.

Key Takeaways for Taxpayers and Professionals

- DRC-01 is only a summary and cannot substitute a proper SCN

- Issuance of SCN under Section 73(1) is mandatory before passing any adverse order

- Unsigned or unauthenticated notices are invalid in the eyes of law

- Personal hearing is compulsory, even if not specifically requested

- Failure to follow due process can render entire proceedings void

Conclusion

This judgment serves as a strong reminder to tax authorities to strictly adhere to statutory procedures. For taxpayers, it provides a valuable precedent to challenge arbitrary or non-compliant GST demands.

The ruling not only strengthens procedural safeguards but also upholds the fundamental principle that justice must not only be done but must also be seen to be done.