The introduction of the Income Tax Act, 2025 marks a significant transformation in India’s taxation framework, particularly in the area of Tax Deducted at Source (TDS). For decades, professionals and businesses have navigated a complex web of multiple TDS provisions under the Income-tax Act, 1961. The new law aims to simplify, consolidate, and modernize this system, making compliance more streamlined and technology-friendly.

From Fragmentation to Consolidation

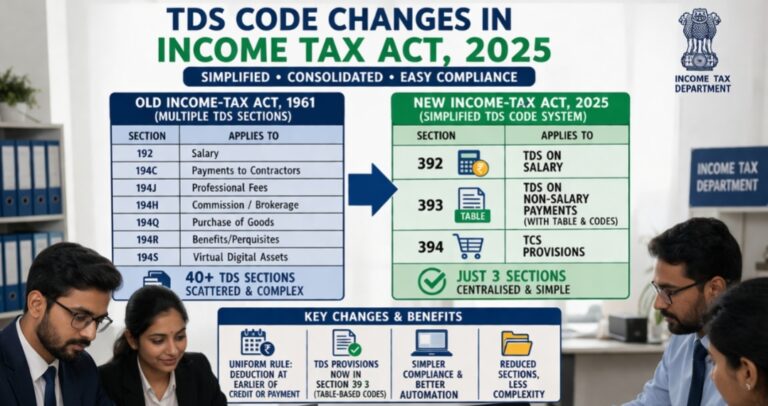

Under the erstwhile regime, TDS provisions were spread across numerous sections such as 192 (salary), 194C (contract payments), 194J (professional fees), and 194H (commission), among many others. This fragmentation often led to interpretational challenges, compliance errors, and increased administrative burden for taxpayers and professionals alike.

The Income Tax Act, 2025 replaces this scattered structure with a consolidated framework. TDS provisions are now primarily housed within a few key sections:

- Section 392 – TDS on Salary

- Section 393 – TDS on Non-Salary Payments

- Section 394 – Tax Collected at Source (TCS)

This consolidation significantly reduces the number of operative provisions and eliminates the need to track multiple sections for different types of payments.

Introduction of a Table-Based Code System

One of the most notable innovations is the introduction of a table-based TDS code system under Section 393. Instead of assigning separate sections to each category of payment, the new framework uses structured tables where various transactions—such as professional fees, rent, commission, and purchase of goods—are categorized under specific codes.

This approach enhances clarity and ensures uniformity in interpretation. It also facilitates easier integration with accounting software and enterprise resource planning (ERP) systems, paving the way for automated compliance.

Uniform Rule for TDS Deduction

Another critical reform is the introduction of a uniform rule for TDS deduction timing. Under the previous regime, the timing of deduction varied across sections—some required deduction at the time of payment, others at the time of credit, and certain provisions had additional complexities.

The new Act standardizes this by mandating that TDS must be deducted at the earlier of credit or payment in all applicable cases. This uniformity reduces ambiguity and minimizes disputes arising from timing differences.

Rationalisation of Provisions and Rates

In addition to structural changes, the Act also rationalizes various TDS provisions and rates. Several redundant or overlapping provisions have been eliminated, and threshold limits have been revised to reduce the compliance burden for smaller transactions.

For instance, the introduction of TDS on partner remuneration under a new provision reflects the government’s intent to widen the tax base while maintaining clarity. Similarly, the removal of higher TDS provisions for non-filers simplifies the compliance landscape and reduces procedural complexities.

Technology-Driven Compliance

The redesigned TDS framework aligns closely with the government’s broader objective of digitisation and ease of doing business. By consolidating provisions and introducing standardized codes, the system becomes more compatible with automated tax compliance tools.

This is expected to reduce manual intervention, minimize errors, and improve the accuracy of TDS reporting. It also enhances transparency and enables better data analytics for tax authorities.

Implications for Tax Professionals and Businesses

For chartered accountants, tax practitioners, and corporate taxpayers, this transition requires a proactive approach. Existing systems and processes must be updated to align with the new structure. Mapping old TDS sections to the new code-based system will be a critical exercise during the transition phase.

Training and awareness will also play a key role in ensuring smooth adoption. While the new framework simplifies compliance in the long run, initial implementation may require adjustments in accounting practices, documentation, and internal controls.

Conclusion

The TDS reforms under the Income Tax Act, 2025 represent a fundamental shift from a fragmented, section-based approach to a consolidated, code-driven system. By simplifying provisions, standardizing rules, and leveraging technology, the new framework aims to enhance efficiency, reduce compliance burden, and improve the overall taxpayer experience.

For professionals and businesses, this change is not merely procedural but transformative, signaling a move towards a more modern and streamlined tax administration system in India.