The Income Tax Department has approached the Supreme Court challenging a significant Delhi High Court judgment that quashed reassessment proceedings initiated against NDTV founders Dr. Prannoy Roy and Radhika Roy. The case concerns interest-free loans allegedly received from RRPR Holdings Private Limited and raises important questions regarding the limits of reassessment powers under the Income Tax Act.

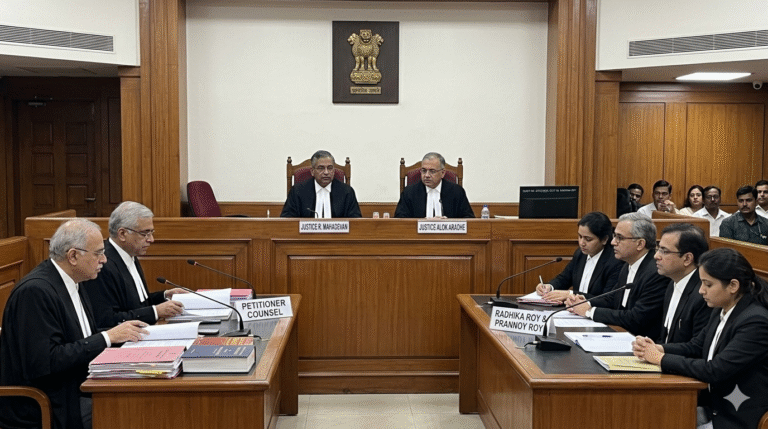

The matter, titled The Deputy Commissioner of Income Tax vs. Radhika Roy (Diary No. 34735/2026), is expected to be listed before a vacation bench comprising Justices R. Mahadevan and Alok Aradhe on June 30, 2026.

Background of the Tax Dispute

The dispute originated from financial transactions involving RRPR Holdings Pvt. Ltd., a company associated with the NDTV promoters. According to the Income Tax Department, RRPR had extended interest-free loans amounting to approximately ₹21 crore to Dr. Prannoy Roy and around ₹71 crore to Radhika Roy.

Tax authorities alleged that these transactions resulted in taxable benefits under the provisions of the Income Tax Act because RRPR itself had borrowed funds from ICICI Bank at an interest rate of approximately 19% and subsequently advanced interest-free loans to the individuals.

However, the controversy does not merely revolve around the taxability of these transactions but rather whether the Department could reopen assessments multiple times on the same set of facts.

Earlier Reassessment Proceedings and Examination

The case records indicate that the Income Tax Department had already initiated reassessment proceedings in 2011 concerning the same transactions.

During those proceedings, the Department reportedly examined the interest-free loans in detail and sought explanations and supporting documents from the taxpayers. The matter concluded with an assessment order dated March 30, 2013.

Importantly, despite conducting scrutiny, the Department did not make any addition or adverse finding regarding the loans at that stage.

Subsequently, in March 2016, fresh reassessment notices under Section 148 of the Income Tax Act were issued again for Assessment Year 2009–10. This time, authorities claimed that the earlier transactions represented taxable benefits requiring reassessment.

This second round of reassessment became the focal point of the legal challenge.

Delhi High Court Quashes Reassessment Notices

In its judgment delivered on January 16, 2026, the Delhi High Court strongly criticised the Department’s attempt to reopen the issue.

A Division Bench consisting of Justices Dinesh Mehta and Vinod Kumar held that the reassessment proceedings were unsustainable because the underlying transaction had already been examined during earlier reassessment proceedings.

The Court observed that all relevant financial records, including RRPR’s books of accounts and transaction documents, had previously been scrutinised.

According to the High Court, initiating fresh proceedings on identical material amounted to an impermissible “change of opinion,” which is not permitted under settled tax jurisprudence.

The Court further held that repeated reopening of completed assessments on the same facts violated constitutional protections and exceeded statutory jurisdiction.

In a strongly worded observation, the Court stated that subjecting taxpayers to reassessment for the same transaction and substantially the same issue was arbitrary and unconstitutional, offending rights guaranteed under Articles 14, 19(1)(g), and 300A of the Constitution of India.

Consequently, the Court quashed the reassessment notices along with all consequential proceedings and imposed costs of ₹1 lakh each in favour of the petitioners.

Income Tax Department Approaches Supreme Court

Unhappy with the High Court’s decision, the Income Tax Department has now filed a Special Leave Petition (SLP) before the Supreme Court seeking restoration of reassessment proceedings.

The Supreme Court’s decision may become important for determining the boundaries of reassessment powers under the Income Tax Act and clarifying whether tax authorities can revisit issues that were previously examined and consciously accepted.

Notably, this is not the first setback for the Department in related litigation.

On April 2, 2026, the Supreme Court had reportedly dismissed another appeal filed by the Department against a separate Delhi High Court judgment that had similarly quashed reassessment proceedings involving RRPR Holdings Pvt. Ltd.

Why This Case Matters

This litigation could have wider implications for taxpayers and tax administration in India. The outcome may influence future disputes involving reopening of completed assessments and reinforce judicial scrutiny over repeated reassessment attempts.

Tax professionals and businesses will closely watch the Supreme Court proceedings, as the ruling may further define the balance between revenue collection powers and taxpayer certainty under Indian tax law.

Case Title: The Deputy Commissioner of Income Tax vs. Radhika Roy

Case Number: Diary No. 34735/2026

Follow the Link below to watch the video: