In a significant ruling concerning income tax reassessment proceedings, the Bombay High Court has clarified that a reassessment notice cannot be treated as having been issued merely because it was digitally signed on March 31, 2021. If the notice was actually dispatched through the Income Tax Business Application (ITBA) portal and received by the taxpayer on April 1, 2021, it will be deemed to have been issued on April 1, 2021. Consequently, such proceedings must comply with the new reassessment framework introduced by the Finance Act, 2021.

The judgment was delivered by a Division Bench comprising Justice B.P. Colabawalla and Justice Firdosh P. Pooniwalla in the case of Shreenath Finstock Private Ltd. v. Union of India & Others (Writ Petition No. 3526 of 2022). The decision reinforces the importance of the actual date of issuance and communication of a reassessment notice rather than the date appearing on the notice itself.

Background of the Case

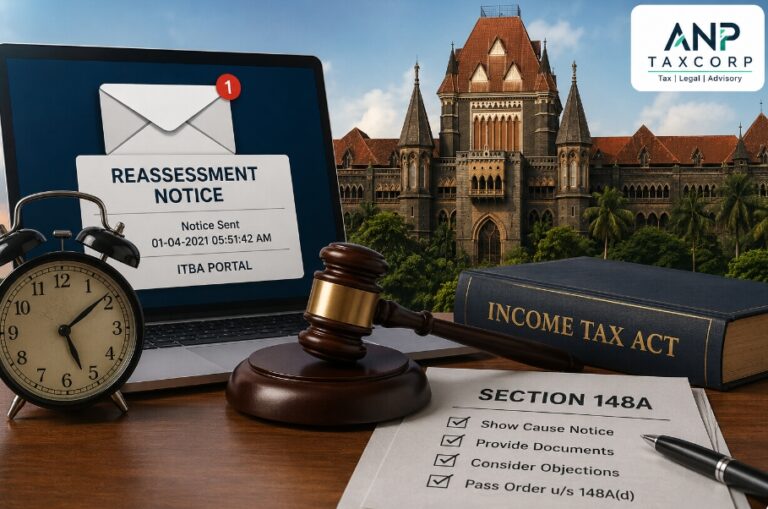

The dispute arose in relation to Assessment Year (AY) 2013-14. The Income Tax Department issued a reassessment notice under the old provisions of the Income Tax Act. Although the notice was dated and digitally signed on March 31, 2021, the taxpayer, Shreenath Finstock Private Limited, received it only on April 1, 2021 through an email generated by the ITBA portal.

The petitioner challenged both the reassessment notice and the consequential assessment order. It argued that since the notice was communicated only on April 1, 2021, the reassessment proceedings were required to follow the amended provisions introduced by the Finance Act, 2021, which came into force from that date.

The Finance Act, 2021 substantially overhauled the reassessment mechanism under the Income Tax Act by introducing safeguards such as the issuance of a show-cause notice under Section 148A, consideration of the assessee’s reply, and passing a reasoned order before initiating reassessment proceedings.

Revenue’s Stand

The Income Tax Department contended that the reassessment notice had been digitally signed and uploaded on the ITBA portal on March 31, 2021. According to the Revenue, once the notice was uploaded on the portal, the Assessing Officer had no further control over the system-generated process of communication.

The Department further argued that the email sent to the taxpayer was merely an additional precautionary step. Therefore, the relevant date for determining the validity of the notice should be the date on which it was uploaded on the ITBA portal and not the date on which the email was generated and delivered to the assessee.

In essence, the Revenue sought to bring the notice within the scope of the old reassessment regime that existed before April 1, 2021.

Court Examines ITBA Portal Records

During the proceedings, the Bombay High Court directed the Department to disclose the precise time at which the ITBA system triggered the communication of the notice.

Based on instructions received from the Assessing Officer, the Revenue informed the Court that the ITBA portal recorded the “Notice Sent” timestamp at 5:51:42 a.m. on April 1, 2021, while the notice was delivered to the taxpayer at 5:51:47 a.m. on April 1, 2021.

After examining these records, the Court observed that there was no dispute regarding the actual date of transmission of the notice. The email communication originated from the ITBA portal only on April 1, 2021, and was received by the assessee on the same day.

The Court therefore concluded that the reassessment notice could not be treated as having been issued on March 31, 2021 merely because it was digitally signed on that date.

Reliance on Earlier Judicial Precedents

While deciding the matter, the Bombay High Court relied upon several important judicial precedents.

A key reference was made to the Delhi High Court’s decision in Suman Jeet Agarwal v. Income Tax Officer, which categorized reassessment notices based on the date of signing and the date of actual communication. The Court found that the present case squarely fell under “Category C,” which covers notices that were dated and digitally signed on or before March 31, 2021 but were actually dispatched and received on or after April 1, 2021.

The Bench also relied on its earlier judgment in Jose Kattadyil Joseph v. Assistant Commissioner of Income Tax, where similar principles regarding the issuance of notices were discussed.

Further support was drawn from the landmark Supreme Court judgment in Union of India v. Ashish Agarwal, which addressed the transition from the old reassessment regime to the new framework introduced by the Finance Act, 2021.

Court’s Findings

The Bombay High Court held that the crucial factor for determining the applicability of the reassessment regime is the actual issuance and communication of the notice to the taxpayer.

Since the notice in the present case was dispatched and received only on April 1, 2021, it was deemed to have been issued on that date. As a result, the reassessment proceedings could not continue under the old provisions of the Income Tax Act.

The Court emphasized that procedural compliance under the amended law was mandatory and could not be bypassed merely because the notice carried an earlier date or had been digitally signed before the new provisions came into force.

Relief Granted by the Court

Based on its findings, the Bombay High Court set aside the consequential assessment order passed against the petitioner.

The Court directed that the impugned reassessment notice should be treated as a show-cause notice under Section 148A(b) of the Income Tax Act. It further instructed the Assessing Officer to provide the assessee with all documents, evidence, and materials relied upon for reopening the assessment.

The taxpayer must be given an opportunity to submit objections, after which the Assessing Officer is required to consider the response and pass a fresh order under Section 148A(d) in accordance with law.

Significance of the Judgment

This ruling provides important clarity regarding reassessment notices issued during the transition period between the old and new reassessment regimes. The judgment confirms that the actual date of dispatch and communication of a notice is decisive in determining whether the old law or the amended provisions apply.

For taxpayers who received reassessment notices around March 31 and April 1, 2021, the decision may offer significant relief where notices were digitally signed before April 1, 2021 but were communicated only after the new law came into effect.

The ruling also reinforces the principle that taxpayers are entitled to the procedural safeguards introduced by the Finance Act, 2021, including disclosure of material relied upon by the Department and an opportunity to be heard before reassessment proceedings are initiated.

Case Title: Shreenath Finstock Private Ltd. v. Union of India & Ors.

Case Number: Writ Petition No. 3526 of 2022