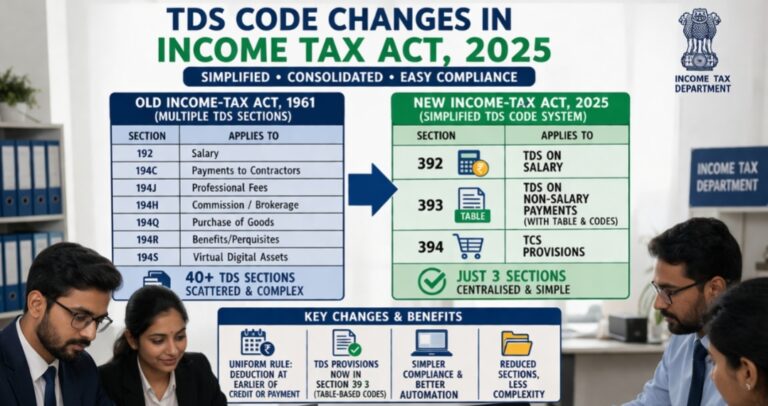

TDS Code Changes under the New Income Tax Act, 2025: A Paradigm Shift in Compliance

The introduction of the Income Tax Act, 2025 marks a significant transformation in India’s taxation framework, particularly in the area of Tax Deducted at Source (TDS). For decades, professionals and businesses have navigated a complex web of multiple TDS provisions under the …