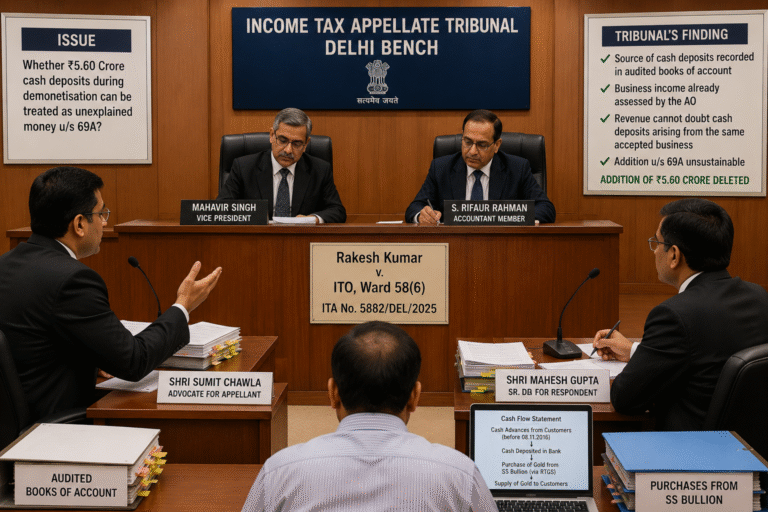

In a significant ruling on demonetisation-related income tax disputes, the Delhi Bench of the Income Tax Appellate Tribunal (ITAT) has deleted an addition of ₹5.60 crore made under Section 69A of the Income Tax Act against a Delhi-based jeweller. The Tribunal held that once cash deposits are duly recorded in audited books of account and corresponding business income has already been assessed, such deposits cannot subsequently be treated as unexplained money.

The decision reinforces an important principle in tax jurisprudence—where business receipts are properly disclosed and accepted during assessment, the Revenue cannot take contradictory positions regarding the same transactions.

Background of the Dispute

The case involved Rakesh Kumar, proprietor of R.V. Gold Hallmark, who had deposited ₹5.60 crore in cash during the demonetisation period following the withdrawal of specified bank notes announced on November 8, 2016.

According to the taxpayer, the deposited amount represented advance payments received in cash from customers before demonetisation for the purchase of gold bullion. The assessee explained that the deposited cash was subsequently used to purchase gold bullion from SS Bullion through RTGS banking transactions, and the purchased bullion was later delivered to customers.

However, the Income Tax Department questioned the genuineness of these transactions.

Assessing Officer’s Findings

During assessment proceedings, the Assessing Officer rejected the explanation offered by the assessee and treated the entire cash deposit of ₹5.60 crore as unexplained money under Section 69A.

The officer observed that:

- Summons issued to certain customers remained unanswered.

- The assessee failed to provide sufficient confirmation from customers who allegedly paid advances.

- VAT returns relating to the transactions had not been filed.

- The claimed business activities lacked adequate verification.

Based on these observations, the Revenue concluded that the taxpayer failed to establish the legitimacy of the source of cash deposits.

First Appellate Authority Upholds Addition

The Commissioner of Income Tax (Appeals) also ruled against the taxpayer and sustained the addition.

According to the appellate authority, the assessee had not demonstrated regular business operations and had failed to substantiate the receipt of customer advances through adequate documentary evidence.

As a result, the addition remained intact until the matter reached the ITAT.

Assessee’s Arguments Before the Tribunal

Before the Tribunal, the taxpayer argued that all transactions were genuine and properly recorded.

The key submissions included:

- Purchases from SS Bullion were executed through banking channels.

- Books of account were regularly maintained and duly audited.

- Cash deposits were reflected in accounting records.

- Customer advances formed part of ordinary business transactions.

- Corresponding purchases and sales were recorded in the books.

The assessee contended that the Revenue had already accepted the business income and therefore could not selectively dispute the source of deposits.

Tribunal’s Observations

After reviewing the material available on record, the ITAT noted that the assessee had maintained audited books of account along with supporting records such as cash books and cash memos.

The Tribunal acknowledged that purchases and corresponding sales had been disclosed in the books.

Although the Bench observed that VAT compliance records and certain sales documentation were not adequately produced, it clarified that such issues fall within the domain of VAT authorities and not income tax authorities while determining taxable income.

Importantly, the Tribunal highlighted a contradiction in the Revenue’s approach.

The Bench observed that on one hand, the Assessing Officer accepted the business income declared by the assessee, while on the other hand questioned the cash deposits arising from the same business transactions.

The Tribunal found this approach legally unsustainable.

Section 69A Addition Held Unsustainable

The Tribunal ultimately held that the source of cash deposits had already been explained through audited books of account and business records.

Since the business income arising from those transactions had already been assessed, making a separate addition under Section 69A would effectively amount to double consideration of the same receipts.

Accordingly, the ITAT deleted the entire addition of ₹5.60 crore and allowed the taxpayer’s appeal.

Key Takeaway

This ruling provides important guidance in demonetisation-era tax litigation. Where cash deposits are properly reflected in audited books and linked to disclosed business activity, tax authorities may face difficulty sustaining additions merely based on suspicion or procedural deficiencies unrelated to income determination.

The judgment also underlines that once business income is accepted, the Revenue must maintain consistency and cannot simultaneously treat the same receipts as unexplained cash.

Case Title: Rakesh Kumar v. ITO, Ward 58(6)

Case Number: ITA No. 5882/DEL/2025

Follow the Link below to watch the video: