The recent decision of the Delhi High Court in MakeMyTrip (India) Pvt. Ltd. v. DCIT serves as a significant reminder of the importance of reasoned decision-making by tax authorities, especially in matters involving applications for lower or nil tax deduction at source (TDS).

Background of the Case

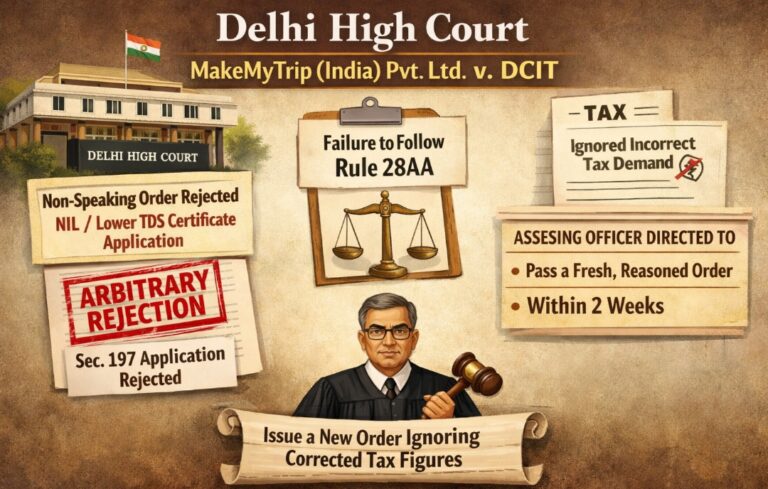

The case revolved around an application filed by MakeMyTrip under Section 197 of the Income-tax Act, 1961. This provision allows a taxpayer to seek a certificate from the Assessing Officer (AO) for deduction of tax at a lower rate or for no deduction at all, depending on the taxpayer’s estimated income and tax liability. Such applications are crucial for businesses, particularly those dealing with high-volume transactions, as excessive TDS can severely impact cash flow and working capital.

In this instance, the company approached the tax authorities seeking a NIL or lower TDS certificate. However, the application was rejected by the AO through a brief and non-speaking order—one that did not provide adequate reasons or justification for the decision.

Key Issues Before the Court

The primary issue before the court was whether the rejection of the application complied with the procedural and substantive requirements laid down under the law, particularly Rule 28AA, which governs the manner in which such applications should be evaluated.

Rule 28AA mandates that the Assessing Officer must consider various factors such as:

- The estimated income of the applicant

- Tax payable on such income

- Existing tax liabilities

- Past tax payments and compliance history

The petitioner argued that the AO had failed to properly consider these parameters and had instead relied on incorrect or outdated tax demand figures, leading to an arbitrary rejection of the application.

Observations of the Delhi High Court

The Delhi High Court took a critical view of the manner in which the AO had handled the application. It emphasized that administrative and quasi-judicial authorities are obligated to pass reasoned orders, particularly when their decisions have financial consequences for taxpayers.

The court noted that the impugned order was a “non-speaking order,” meaning it lacked clarity, reasoning, and transparency. Such orders fail to demonstrate application of mind and are liable to be set aside on that ground alone.

Importantly, the court also found merit in the taxpayer’s contention that incorrect tax demand figures had been considered. This indicated not only procedural lapses but also a failure to verify relevant facts before arriving at a decision.

Legal Principles Reinforced

This judgment reinforces several key legal principles:

- Requirement of Reasoned Orders

Authorities must provide clear and cogent reasons for their decisions. A mere rejection without explanation is not sustainable in law. - Adherence to Prescribed Rules

The procedure under Rule 28AA is not optional. The AO must strictly follow the prescribed criteria while evaluating applications under Section 197 of Income Tax Act. - Fairness and Non-Arbitrariness

Any decision affecting a taxpayer’s rights must be fair, reasonable, and based on accurate data. Arbitrary actions undermine trust in the tax administration system.

Court’s Direction

In light of these findings, the Delhi High Court set aside the impugned order and directed the Assessing Officer to reconsider the application. The AO was instructed to:

- Pass a fresh, reasoned order

- Properly apply the parameters under Rule 28AA

- Ignore incorrect or disputed tax demand figures

- Complete the exercise within a strict timeline of two weeks

Practical Implications for Taxpayers

This ruling is particularly relevant for businesses that regularly apply for lower or NIL TDS certificates. It highlights that:

- Taxpayers have the right to challenge arbitrary or unreasoned rejections

- Proper documentation and accurate representation of tax liability are crucial

- Courts are willing to intervene where procedural fairness is compromised

For tax professionals and advisors, the judgment underscores the importance of scrutinizing orders passed by tax authorities and ensuring that due process has been followed.

Conclusion

The decision in MakeMyTrip (India) Pvt. Ltd. v. DCIT strengthens the principle that tax administration must operate within the bounds of fairness, transparency, and accountability. By setting aside a non-speaking and arbitrary order, the Delhi High Court has reaffirmed that procedural compliance is not a mere formality but a fundamental requirement in tax adjudication.