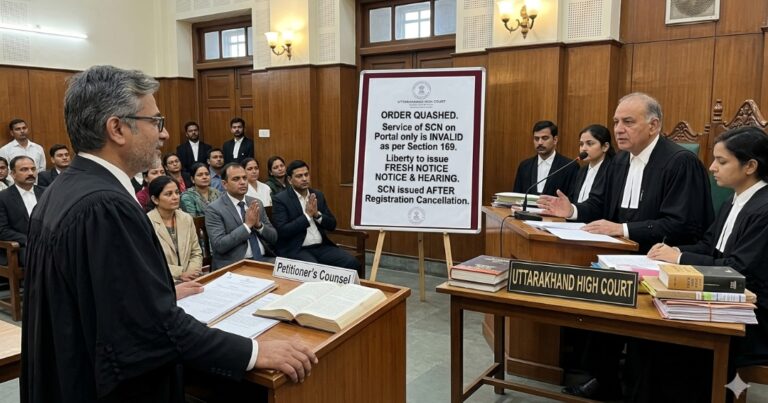

The Uttarakhand High Court has delivered a landmark ruling that reinforces the principles of natural justice within the GST framework.

In the case of [2026] 184 taxmann.com 346 (Uttarakhand), the Court quashed a tax demand order on the grounds that a Show Cause Notice (SCN) served solely through the digital portal—after a taxpayer’s registration was cancelled—is legally invalid under Section 169 of the CGST/UKGST Act.

The Core Dispute: Portal Service vs. Notice Accessibility

The petitioner, a taxpayer whose GST registration had been cancelled by the department, was subsequently issued a Show Cause Notice regarding tax liabilities. The tax authorities uploaded this SCN to the GST portal’s “Additional Notices and Orders” section.

When the petitioner failed to respond to the digital notice, the department proceeded to pass an ex-parte order, creating a significant tax demand. The petitioner challenged this, arguing they had no knowledge of the notice because they had stopped checking the portal regularly once their business registration was officially cancelled.

The High Court’s Findings

The Uttarakhand High Court meticulously examined the provisions of Section 169 of the CGST Act, which outlines the prescribed modes for service of notice. The Court’s decision centered on three critical observations:

- Ineffectiveness Post-Cancellation: The Court recognized the practical reality that once a GST registration is cancelled, a taxpayer is no longer an active user of the portal for day-to-day compliance. Expecting a person to monitor a “cancelled” account for “additional notices” is unreasonable.

- Section 169 Compliance: While the law allows for digital service, it must be effective. The Court noted that when the primary means of digital communication (the active portal link) is effectively severed by the cancellation of registration, the department should resort to other modes prescribed under Section 169, such as registered post or email to the taxpayer’s last known address.

- Violation of Natural Justice: By failing to ensure the taxpayer actually received the notice, the department denied them the “Right to be Heard.” This procedural lapse rendered the subsequent demand order legally unsustainable.

The Verdict:

Order Quashed with Liberty

The High Court quashed the assessment order, providing immediate relief to the petitioner. However, the Court balanced this by granting the tax department liberty to issue a fresh notice. This ensures that while the taxpayer’s rights are protected, the revenue’s right to investigate potential tax dues remains intact—provided they follow due process.

The Court directed that:

- A fresh notice must be served through a valid mode that ensures the petitioner is actually informed.

- A proper personal hearing must be granted before any new order is passed.

Significance for Taxpayers

This ruling is a significant victory for GST practitioners and businesses. It establishes a clear precedent that the tax department cannot rely on “buried” portal notifications as a shield for lack of communication, especially when the taxpayer’s status has changed. It emphasizes that procedural fairness is not a formality but a mandatory requirement for tax administration.

For businesses with cancelled registrations, this serves as a reminder to maintain updated contact information (email and mobile) with the department, while for the authorities, it serves as a directive to ensure that the “service of notice” is substantive and not merely a “check-box” exercise on a digital dashboard.