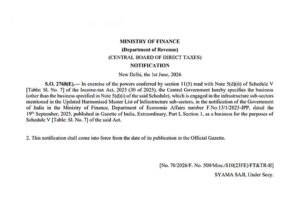

Notification No.: 70/2026/F.No. 500/Misc./S10(23FE)/FT&TR-II

Date: 1 June 2026

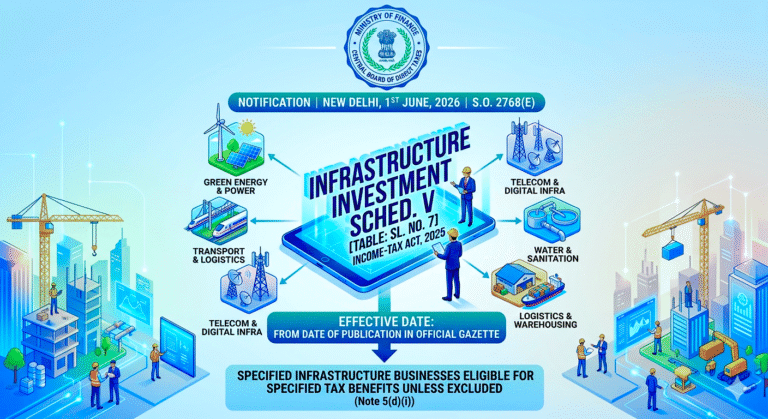

The Ministry of Finance, through the Central Board of Direct Taxes (CBDT), has issued Notification No. 70/2026 specifying certain infrastructure sub-sector businesses as eligible entities under the Income-tax Act, 2025.

Legal Authority

This notification has been issued in exercise of the powers conferred under Section 11(5) read with Note 5(d)(ii) of Schedule V [Table: Sl. No. 7] of the Income-tax Act, 2025.

Scope of Notification

The Central Government has specified that:

- Businesses engaged in infrastructure sub-sectors included in the Updated Harmonised Master List of Infrastructure sub-sectors (as notified by the Ministry of Finance, Department of Economic Affairs vide F.No. 13/1/2025-IPP dated 19 September 2025) shall qualify as eligible businesses.

- This classification enables such entities to fall within the ambit of Schedule V for the relevant tax provisions.

Exclusions

- The notification excludes businesses already covered under Note 5(d)(i) of Schedule V.

- Accordingly, only those infrastructure businesses not previously specified are covered under this notification.

Effective Date

- The notification is effective from 1 June 2026, being the date of its publication in the Official Gazette.

Key Takeaway

This notification provides clarity on the treatment of infrastructure sub-sector businesses and is likely to encourage structured investments into infrastructure by aligning them with the specified tax framework under the Income-tax Act, 2025.

Find below the Copy of the Official Notification by CBDT:

Follow the Link below to Watch the video: