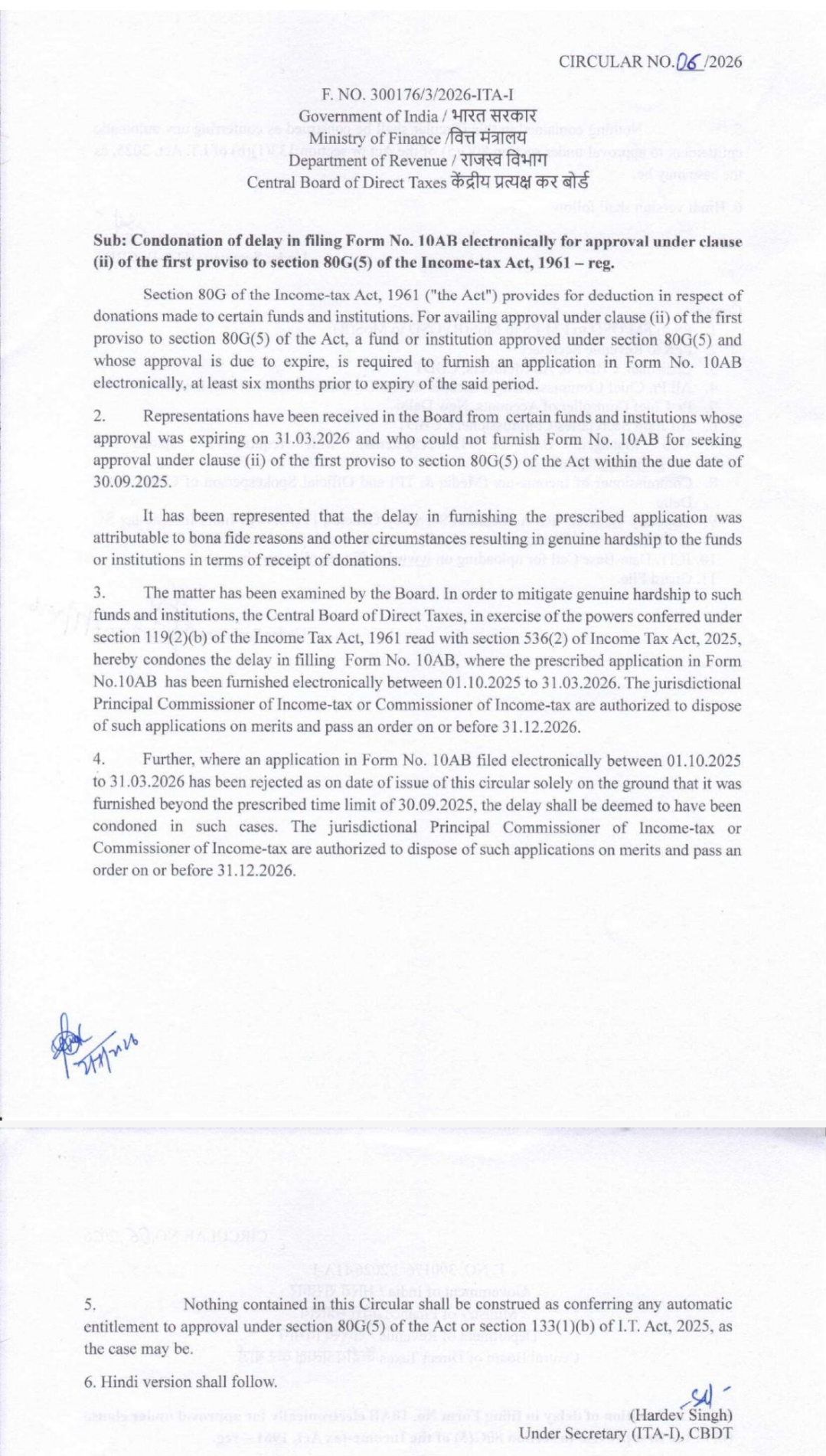

In a significant relief for charitable trusts, funds, and institutions, the Central Board of Direct Taxes (CBDT) has issued Circular No. 06/2026 dated. 2 July 2026, granting condonation of delay in filing Form No. 10AB for renewal of approval under Section 80G(5) of the Income-tax Act, 1961. The circular addresses genuine hardships faced by organizations that could not submit their applications within the prescribed deadline.

Under Section 80G of the Income-tax Act, donors are entitled to claim deductions for donations made to eligible charitable institutions. To continue enjoying this benefit, organizations whose approval under Section 80G was due to expire were required to file an electronic application in Form No. 10AB at least six months before the expiry of the approval period. For approvals expiring on 31 March 2026, the due date for filing Form 10AB was 30 September 2025.

However, the CBDT received several representations from charitable institutions stating that they could not comply with the deadline due to bona fide reasons and circumstances beyond their control. These delays, they submitted, resulted in genuine hardship by adversely affecting their ability to receive donations.

Considering these representations, the CBDT has exercised its powers under Section 119(2)(b) of the Income-tax Act, 1961, read with Section 536(2) of the Income Tax Act, 2025, to condone the delay in filing Form No. 10AB. The relief applies to applications that were filed electronically during the period 1 October 2025 to 31 March 2026.

The circular authorizes the jurisdictional Principal Commissioner of Income-tax (PCIT) or Commissioner of Income-tax (CIT) to examine such delayed applications on their merits and pass appropriate orders on or before 31 December 2026.

The CBDT has also provided relief to applicants whose Form No. 10AB applications were already rejected solely because they were filed after the prescribed due date. In such cases, the delay shall now be deemed to have been condoned, and the concerned tax authorities have been directed to reconsider these applications on merits within the same deadline of 31 December 2026.

Importantly, the circular clarifies that condonation of delay does not automatically entitle any institution to approval under Section 80G(5) of the Income-tax Act, 1961, or the corresponding provisions of the Income Tax Act, 2025. Every application will continue to be scrutinized on its merits before approval is granted.

This circular offers timely relief to genuine charitable organizations by ensuring that procedural delays alone do not deprive them of the opportunity to renew their tax-exempt status and continue attracting tax-deductible donations.

Find the Circular here:

Follow the Link below to watch the video: