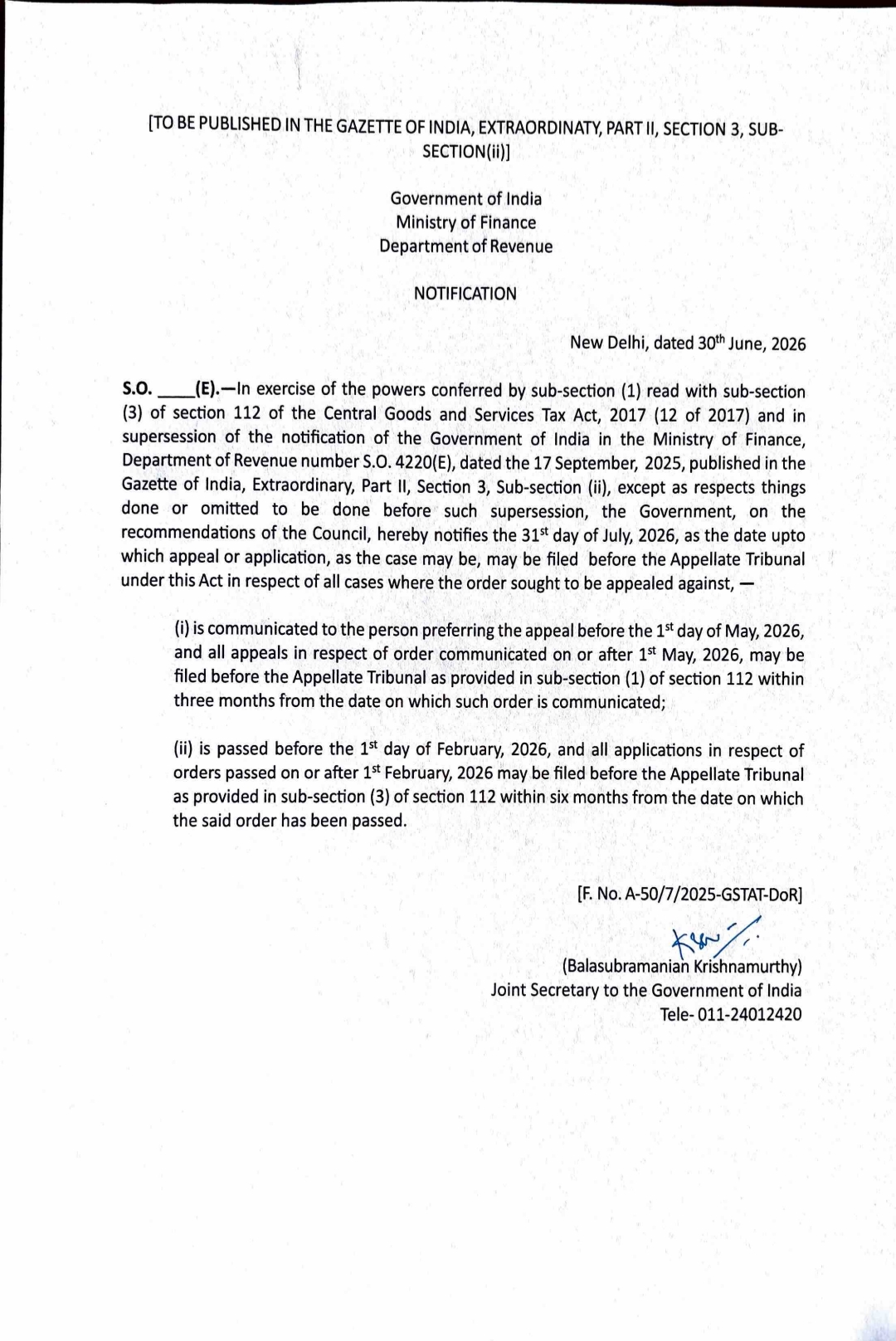

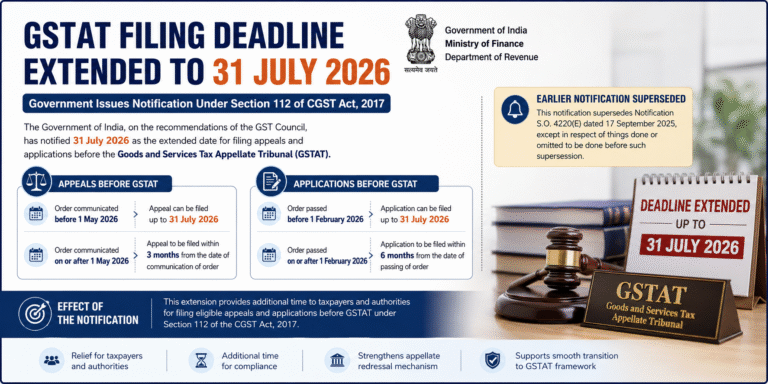

In a significant relief for taxpayers and tax authorities, the Government of India, Ministry of Finance, Department of Revenue, has issued a fresh notification extending the timeline for filing appeals and applications before the Goods and Services Tax Appellate Tribunal (GSTAT).

Through Notification dated 30 June 2026, the Central Government has notified 31 July 2026 as the revised last date for filing eligible appeals and applications under Section 112 of the Central Goods and Services Tax (CGST) Act, 2017.

The notification has been issued in exercise of powers under Section 112(1) read with Section 112(3) of the CGST Act, based on the recommendations of the GST Council.

Earlier Notification Superseded

With this development, the Government has superseded the earlier Notification S.O. 4220(E) dated 17 September 2025, while protecting actions already taken or omitted before the replacement of the earlier notification.

Revised Time Limit for Filing Appeals Before GSTAT

The notification provides a structured filing timeline depending on the date of communication of the order:

1. Orders Communicated Before 1 May 2026

Where the order proposed to be challenged was communicated to the appellant before 1 May 2026, the appeal before GSTAT can now be filed up to 31 July 2026.

2. Orders Communicated On or After 1 May 2026

For orders communicated on or after 1 May 2026, the normal statutory timeline under Section 112(1) of the CGST Act will apply, allowing filing within three months from the date of communication of the order.

Revised Time Limit for Filing Applications Before GSTAT

Separate timelines have also been prescribed for applications:

1. Orders Passed Before 1 February 2026

Where the relevant order was passed before 1 February 2026, applications before the Appellate Tribunal may be filed up to 31 July 2026.

2. Orders Passed On or After 1 February 2026

For orders passed on or after 1 February 2026, applications will continue to be governed by Section 112(3) of the CGST Act, allowing filing within six months from the date of passing of the order.

Impact of the Notification

This extension offers additional time to taxpayers and authorities to pursue appellate remedies before GSTAT and ensures smoother transition into the tribunal-based dispute resolution framework under GST law.

Eligible taxpayers who were unable to file appeals or applications earlier should review the applicability of the revised deadlines and take necessary action before 31 July 2026.

Find the Official Notification here: