India’s direct tax landscape is undergoing a historic transformation with the introduction of the Income Tax Act, 2025, set to take effect from April 1, 2026 (FY 2026–27). Replacing the decades-old Income Tax Act, 1961, the new legislation aims to simplify tax laws, reduce litigation, and promote voluntary compliance while aligning with global best practices.

This reform is not merely cosmetic—it represents a structural reset of how taxation is understood, administered, and complied with in India.

A Simpler, Structured Tax Code

One of the most notable features of the new Act is its streamlined structure and simplified language. Over the years, the 1961 Act had become complex, filled with provisos, explanations, and cross-references that often led to disputes and confusion.

The 2025 Act reorganizes provisions into a more logical and concise format, eliminating redundancy and improving readability. This is expected to significantly reduce interpretational issues and litigation, benefiting both taxpayers and professionals.

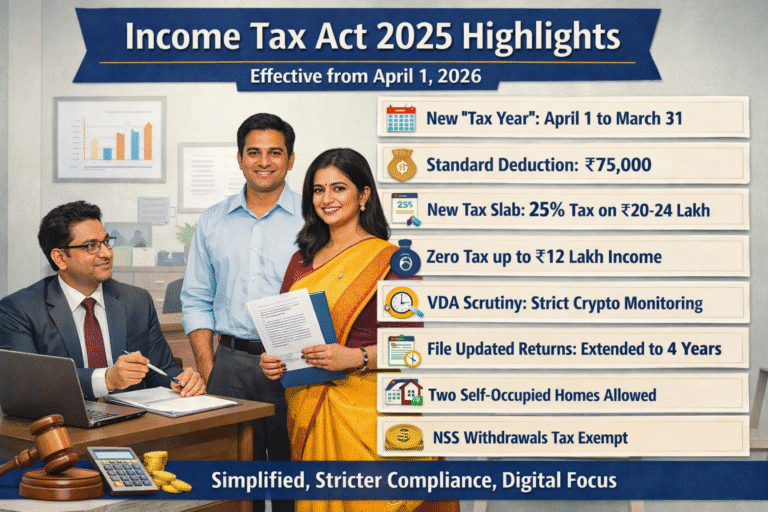

Introduction of the “Tax Year” Concept

A major conceptual shift is the replacement of the “Previous Year” and “Assessment Year” with a single “Tax Year”, running from April 1 to March 31.

This change removes long-standing confusion, especially among new taxpayers, and aligns India’s tax system with international practices. It simplifies return filing, advisory, and compliance processes, making the system more intuitive.

New Tax Regime as the Default System

The Act reinforces the new tax regime as the default option, requiring taxpayers to actively opt out if they wish to continue under the old regime.

This regime follows a low-tax, minimal-deduction approach, where most traditional deductions such as those under Sections 80C, 80D, and HRA are not available. The idea is to simplify compliance and reduce dependency on tax-saving investments.

Revised Tax Slabs and Increased Standard Deduction

The government has introduced a new 25% tax slab for income between ₹20 lakh and ₹24 lakh, making the tax structure more progressive.

Additionally, the standard deduction has been increased to ₹75,000 for salaried individuals and pensioners. This directly reduces taxable income and enhances disposable income, especially for the middle class.

Enhanced Rebate under Section 87A

A significant relief measure is the extension of the rebate under Section 87A, ensuring zero tax liability for individuals with income up to ₹12 lakh.

This move is expected to boost compliance and provide substantial relief to a large segment of taxpayers.

Rationalization of TDS/TCS Provisions

To reduce compliance burden, the Act consolidates Tax Deducted at Source (TDS) provisions into a single section (Section 393).

This simplification minimizes confusion arising from multiple sections and improves ease of compliance for businesses and professionals.

Relief in House Property Taxation

The Act provides notable relief for homeowners by allowing up to two properties to be treated as self-occupied, with NIL annual value, irrespective of the reason for non-occupation.

This is a major benefit for taxpayers owning multiple residential properties, significantly reducing their tax burden.

Tax Exemption for NSS Withdrawals

Withdrawals from the National Savings Scheme (NSS) are now fully exempt from tax. This move encourages long-term savings and provides clarity to small investors who previously faced uncertainty regarding taxation.

Higher Deduction for Children’s Education Allowance

Recognizing rising education costs, the Act increases the deduction for children’s education allowance to ₹3,000 per month per child.

This provides meaningful relief to salaried individuals with dependent children and aligns tax policy with current economic realities.

Stricter Regulation of Virtual Digital Assets (VDAs)

With the growing importance of digital assets like cryptocurrencies, the Act introduces stricter provisions:

- VDAs are included in the definition of undisclosed income during search proceedings

- Authorities are empowered to access digital platforms, including email servers, social media accounts, and online wallets

This reflects a shift towards technology-driven tax enforcement and aims to curb tax evasion in the digital economy.

Expanded Powers in Search & Seizure

Search and seizure provisions have been modernized to include access to virtual and cloud-based data.

This marks a significant transition toward data-centric investigations, making it essential for taxpayers to maintain proper digital records and audit trails.

Extended Timeline for Updated Returns

The time limit for filing updated returns has been increased from 2 years to 4 years.

This encourages voluntary compliance by allowing taxpayers to correct errors or omissions without immediate penal consequences, thereby reducing litigation.

Faceless Proceedings and Digital Compliance

The Act strengthens the framework for faceless assessments and appeals, minimizing physical interaction between taxpayers and tax authorities.

This enhances transparency and accountability while emphasizing the importance of accurate documentation and timely digital responses.

Capital Gains and Presumptive Taxation – A Work in Progress

While the Act does not introduce a complete overhaul of capital gains taxation, it signals an intent to simplify classification and reduce disputes, particularly around holding periods and asset categorization.

Similarly, presumptive taxation schemes are expected to continue in a more streamlined manner, benefiting small businesses and professionals by reducing compliance requirements.

Focus on Voluntary Compliance and Reduced Litigation

A key philosophy of the new Act is shifting from a penalty-driven approach to a compliance-driven system. Clear drafting, fewer ambiguities, and extended timelines aim to build trust and encourage honest reporting.

Additionally, many operational aspects are expected to be governed through rules and notifications, allowing flexibility and quicker updates without frequent legislative amendments.

Conclusion

The Income Tax Act, 2025 represents a bold step toward a simpler, more transparent, and technology-driven tax regime. While it reduces complexity and offers tangible relief to taxpayers, it also introduces stricter compliance requirements, especially in the digital space.

For taxpayers and professionals alike, the key to navigating this new regime lies in early understanding, strategic planning, and continuous adaptation. As the law evolves through rules and implementation, staying updated will be critical to leveraging its benefits while ensuring compliance.