A landmark ruling by the Jammu & Kashmir and Ladakh High Court (March 2026) has provided a crucial lifeline for taxpayers who defaulted on payments under the original Direct Tax Vivad Se Vishwas (DTVSV) Act, 2020.

The court clarified that a payment default doesn’t just end the settlement—it completely resets the clock, restoring the legal rights of both the Income Tax Department and the assessee.

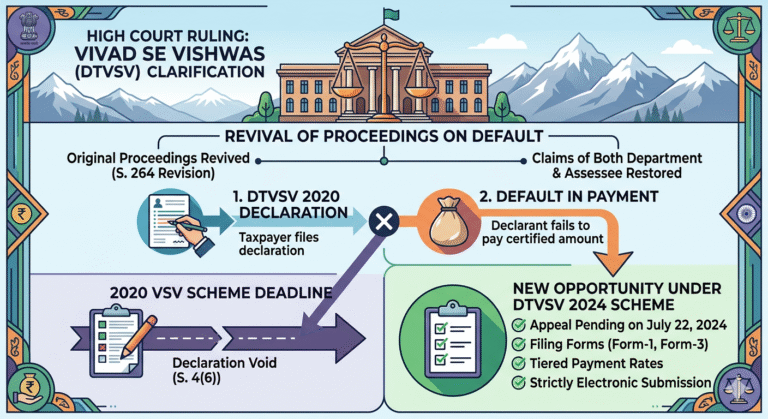

The Core Issue: What Happens After a Default?

Under the 2020 Act, many taxpayers filed declarations to settle disputes but failed to pay the certified amount within the deadline. The Revenue Department argued that while their enforcement proceedings could revive, the taxpayer’s original appeals or revision petitions (under Section 264) remained dead.

The High Court’s Landmark Clarification

The Court rejected the Department’s narrow view, focusing on the “Legal Fiction” created by Section 4(6) of the Act:

- Status Quo Ante: If a declarant fails to pay, the declaration is treated as if it were never made.

- No Discrimination: The “revival of proceedings” applies to all claims, whether initiated by the Department or the taxpayer.

- Revision Petitions Included: Specifically, the court ruled that Section 264 revision petitions filed by an assessee are revived automatically upon default.

A Second Chance: Eligibility for VSV 2024

This ruling is a game-changer for those looking to enter the Direct Tax Vivad Se Vishwas Scheme, 2024.

By “reviving” the original dispute, the court essentially deemed those disputes as “pending” in the eyes of the law. This status allows taxpayers who missed out in 2020 to apply for the 2024 Scheme, provided the revived appeal meets the new cut-off date of July 22, 2024.

Quick Comparison: Moving from 2020 to 2024

| Feature | DTVSV 2020 | DTVSV 2024 |

|---|---|---|

| Pending Date | Must be pending on Jan 31, 2020 | Must be pending on July 22, 2024 |

| Revival Rule | Default = Void Declaration | Default = Legal Restoration |

| Payment Rates | Standard flat rates | Tiered rates (New vs. Old Appellants) |

| Filing Mode | Mixed | Strictly Electronic (Form-1 to Form-4) |

The Bottom Line:

This judgment ensures that a failed 2020 settlement isn’t a dead end. It restores your original legal standing, potentially opening the door to a more favorable settlement under the 2024 Scheme.