The Supreme Court of India recently delivered a landmark judgment in V. Ganesan v. State (2026), fundamentally refining how the law interprets the dishonour of a Post-Dated Cheque (PDC) in relation to the criminal charge of cheating under Section 420 of the Indian Penal Code (IPC).

This ruling provides much-needed clarity for entrepreneurs, film producers, and business owners who frequently use PDCs as a tool for credit and deferred payments.

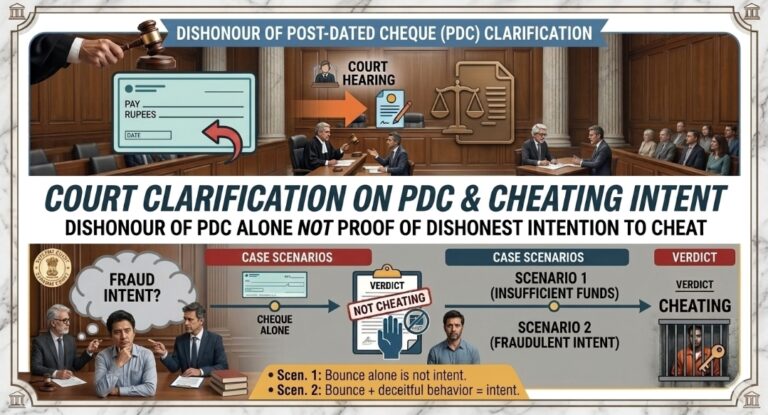

The Core Ruling: Beyond the Bounced Cheque

The central takeaway of the verdict is that the mere dishonour of a post-dated cheque is not sufficient proof of a dishonest intention to cheat. In the eyes of the Court, there is a distinct legal line between a civil breach of contract (or a statutory offense under the Negotiable Instruments Act) and a criminal act of fraud.

To sustain a conviction for cheating under Section 420, the prosecution must prove that the accused had a dishonest or fraudulent intention at the very beginning (inception) of the transaction. If a person issues a PDC with the genuine expectation of having funds later but fails due to business losses or unforeseen circumstances, it cannot be presumed they intended to deceive the other party from the start.

The Case Context: High-Risk Ventures

The ruling arose from a case involving a film producer, V. Ganesan, who issued PDCs to an investor as part of a profit-sharing agreement. When the movie failed to generate the expected returns and the cheques were dishonoured for “insufficient funds,” the investor filed charges of cheating.

The Supreme Court observed that in high-risk industries like cinema, the failure of a project does not automatically make the borrower a criminal. The Court noted that the producer had actually completed the film—demonstrating an effort to fulfill his end of the bargain. Since the cheques were issued to settle a liability arising from a business venture, their dishonour did not, by itself, indicate a “guilty mind” (mens rea) to defraud.

Scenario 1 vs. Scenario 2: Understanding the Difference

The court’s logic can be broken down into two distinct scenarios:

- Scenario 1: Insufficient Funds (Civil/Statutory Liability)

In this case, a person issues a PDC believing funds will be available. If the cheque bounces, it triggers Section 138 of the Negotiable Instruments Act, which is a “strict liability” offense. The focus here is on the recovery of money and maintaining the sanctity of banking transactions. It does not carry the same social or legal stigma as a “cheating” conviction. - Scenario 2: Fraudulent Intent (Criminal Liability)

Cheating occurs when the accused uses the cheque as a tool of inducement to trick the victim into handing over property or money, with no intention of ever paying it back. If there is evidence of deceitful behavior—such as providing a cheque for a closed account or disappearing immediately after the transaction—then Section 420 IPC applies.

Why This Matters for Indian Business

This judgment serves as a vital safeguard against the criminalization of business failures. It prevents disgruntled creditors from using the threat of a “cheating” case—which carries harsher penalties and potential arrest—as a leverage tool for debt recovery when no actual fraud occurred.

By emphasizing the “Inception Rule,” the Supreme Court has ensured that the law protects those who act in good faith but fall victim to market risks, while still leaving the door open to prosecute those who truly intend to defraud.