In a significant ruling, the Income Tax Appellate Tribunal (ITAT), Chennai Bench, has reiterated that reassessment proceedings initiated beyond three years from the end of the relevant assessment year are legally unsustainable if mandatory approval from the competent authority is not obtained.

Key Ruling in the Case

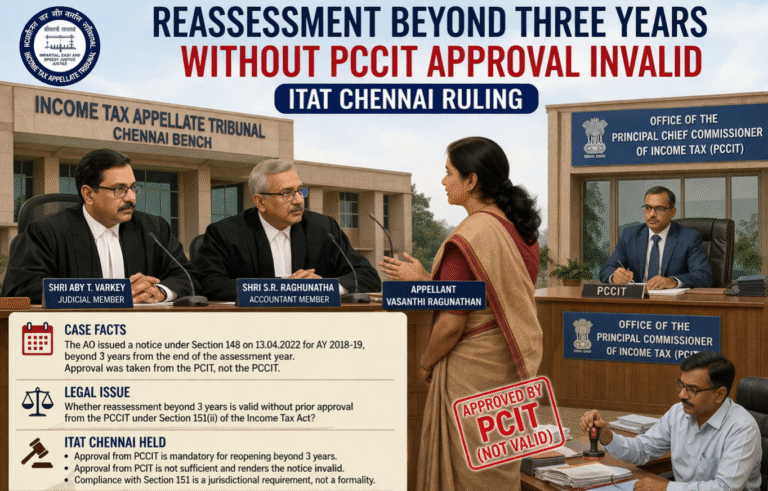

The Tribunal delivered its decision on 25 March in the case of Vasanthi Ragunathan v. ITO (ITA No. 2896/Chny/2025), setting aside reassessment proceedings due to non-compliance with statutory approval requirements under the Income Tax Act.

The Bench, comprising Judicial Member Aby T. Varkey and Accountant Member S.R. Raghunatha, held that the reassessment notice issued under Section 148 was invalid as it lacked proper sanction from the Principal Chief Commissioner of Income Tax (PCCIT).

Background of the Case

In this case, the Assessing Officer (AO) issued a reassessment notice dated 13 April 2022 for Assessment Year 2018–19—clearly beyond the statutory period of three years. However, instead of obtaining approval from the PCCIT as mandated under Section 151(ii), the AO secured approval from the Principal Commissioner of Income Tax (PCIT), Coimbatore.

The assessee challenged the validity of the notice on the ground that approval from the PCIT does not satisfy the legal requirement where reassessment is initiated after three years.

Tribunal’s Observations

The ITAT emphasized that compliance with Section 151 is not merely procedural but a jurisdictional condition. It clarified that:

- For reassessment beyond three years, prior approval must be obtained specifically from the PCCIT.

- Approval from any lower authority, including PCIT, is legally insufficient.

- Failure to comply with this requirement invalidates the entire reassessment process.

The Tribunal categorically observed that the Assessing Officer acted in violation of the statutory mandate by not obtaining approval from the appropriate authority.

Final Verdict

The ITAT Chennai held that the reassessment notice issued under Section 148 was invalid in law, as it was not backed by the requisite approval under Section 151(ii). Consequently:

- The reassessment proceedings were quashed.

- The assessment order arising from such invalid notice was set aside.

Legal Takeaway

This ruling reinforces a crucial principle: jurisdictional requirements under tax law must be strictly complied with. Any deviation—especially in obtaining approvals from the correct authority—can render the entire reassessment void.

Why This Matters

For taxpayers and professionals, this decision highlights:

- The importance of verifying approval hierarchy in reassessment cases.

- A strong ground to challenge reassessment notices issued beyond three years without proper sanction.

- The judiciary’s consistent stance that procedural lapses affecting jurisdiction cannot be cured retrospectively.

Citation: 2026 LLBiz ITAT(CHE) 80

Case: Vasanthi Ragunathan v. ITO Ward

Forum: ITAT Chennai Bench