The Bangalore Bench of the Customs, Excise and Service Tax Appellate Tribunal (CESTAT) has delivered a significant ruling clarifying the scope of Goods Transport Agency (GTA) services under the erstwhile service tax regime. In the case of South Eastern Coalfields Ltd. vs. Commissioner of Central Excise & Service Tax, the Tribunal addressed a recurring issue concerning the taxability of transportation services provided by individual truck operators who do not issue consignment notes.

At the heart of the dispute was whether such transport activities could be classified as GTA services and thereby subjected to service tax. The department had sought to levy service tax under the GTA category, contending that the transportation of goods by road falls squarely within its ambit. However, the assessee argued that the absence of a consignment note fundamentally alters the nature of the service, taking it outside the statutory definition of a Goods Transport Agency.

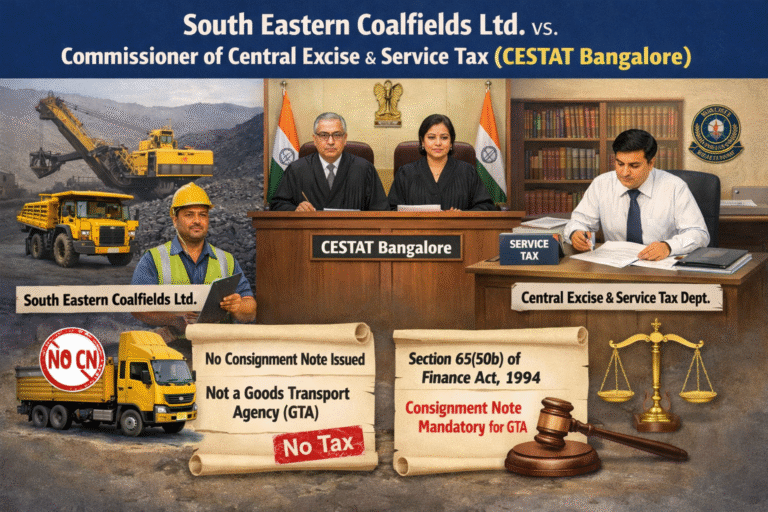

The Tribunal examined the legal framework under Section 65(50b) of the Finance Act, 1994, which defines a “Goods Transport Agency” as any person who provides service in relation to transport of goods by road and issues a consignment note. The issuance of a consignment note is not a mere procedural formality but a substantive requirement that establishes the agency’s responsibility for the goods during transit. It signifies the transfer of custody and liability, thereby distinguishing a GTA from individual transport operators.

In this context, the Tribunal emphasized that the definition is explicit and leaves little room for interpretational ambiguity. The presence of a consignment note is a sine qua non for classifying a service provider as a GTA. Consequently, in the absence of such documentation, the service cannot be brought within the tax net under the GTA category.

Applying this principle to the facts of the case, the Tribunal observed that the transportation services in question were rendered by individual truck operators who did not issue consignment notes. These operators were essentially engaged on a hire basis and did not assume the characteristics or responsibilities of a Goods Transport Agency. There was no evidence to suggest that they undertook the obligations typically associated with a GTA, such as issuing transport documents or assuming liability for the goods.

The Tribunal further noted that merely transporting goods by road does not automatically qualify a service as a GTA service. The statutory definition must be strictly adhered to, and all essential conditions must be satisfied. In the absence of a consignment note, the foundational requirement for classification as a GTA remains unfulfilled.

As a result, the Bangalore Bench held that the services provided by such individual truck operators do not fall within the ambit of GTA services and are therefore not liable to service tax under that category. This ruling reinforces the principle that tax statutes must be interpreted strictly, and no liability can be imposed by extending the scope of a definition beyond its clear terms.

This decision carries important implications for businesses and transporters alike. For companies engaging transport services, it underscores the importance of understanding the nature of the service provider and the documentation involved. For individual truck operators, it provides clarity that in the absence of issuing consignment notes, their services may not attract service tax under the GTA framework.

From a broader perspective, the ruling serves as a reminder of the critical role played by statutory definitions in determining tax liability. It also highlights the judiciary’s consistent approach in upholding the letter of the law, particularly in matters involving classification and taxation. As disputes under the erstwhile service tax regime continue to be adjudicated, such precedents offer valuable guidance for both taxpayers and practitioners navigating similar issues.