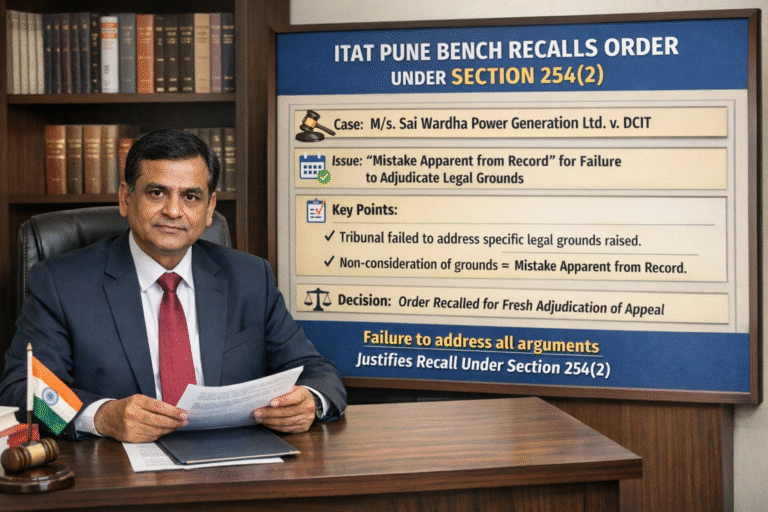

In a significant ruling reinforcing the principles of natural justice, the Income Tax Appellate Tribunal (ITAT), Pune Bench, has reiterated that failure to adjudicate all grounds raised by an assessee constitutes a “mistake apparent from the record,” warranting recall of the order under Section 254(2) of the Income Tax Act, 1961. The decision came in the case of M/s. Sai Wardha Power Generation Ltd. v. DCIT and serves as an important precedent for taxpayers and practitioners alike.

Background of the Case

The assessee, M/s. Sai Wardha Power Generation Ltd., had filed an appeal before the ITAT challenging certain additions and disallowances made by the Assessing Officer. During the course of appellate proceedings, the assessee raised multiple legal grounds, including jurisdictional issues and merits-based contentions. However, when the Tribunal passed its order, it inadvertently failed to deal with some of the crucial grounds raised in the appeal.

Aggrieved by this omission, the assessee filed a Miscellaneous Application (MA) under Section 254(2), contending that the Tribunal’s failure to adjudicate specific grounds amounted to a mistake apparent from the record. The assessee argued that such non-consideration directly affected the fairness and completeness of the judicial decision.

Core Issue

The primary issue before the Tribunal was whether non-adjudication of certain grounds raised by the assessee could be treated as a “mistake apparent from the record” under Section 254(2), thereby justifying recall of the order.

Tribunal’s Observations

The ITAT Pune Bench acknowledged that it is a fundamental duty of an appellate authority to consider and adjudicate every ground raised before it. The Tribunal emphasized that its role is not merely to decide selectively but to provide a comprehensive adjudication of all issues brought on record.

The Bench observed that failure to address a specific ground is not a minor procedural lapse but a substantive error that goes to the root of the matter. Such an omission results in denial of proper hearing and violates the principles of natural justice. Importantly, the Tribunal clarified that a mistake apparent from the record is not confined to clerical or arithmetical errors but also includes failure to consider material facts or legal submissions.

Decision of the Tribunal

Accepting the assessee’s contention, the ITAT held that the omission to adjudicate certain grounds indeed constituted a mistake apparent from the record. Consequently, the Tribunal exercised its powers under Section 254(2) and recalled its earlier order.

The matter was directed to be listed afresh for adjudication, ensuring that all grounds raised by the assessee would be duly considered and decided on merits. This effectively restored the appeal to its original position before the Tribunal.

Legal Significance and Implications

This ruling has far-reaching implications for both taxpayers and tax professionals. It reinforces the principle that justice must not only be done but must also be seen to be done. Any failure by a judicial body to consider relevant arguments can undermine the integrity of the decision-making process.

From a procedural standpoint, the decision clarifies the scope of Section 254(2). While the provision is often invoked for rectification of apparent errors, this case highlights that its ambit extends to situations where the Tribunal has failed to address key issues altogether.

For practitioners, this serves as a crucial reminder to carefully review ITAT orders to ensure that all grounds have been adjudicated. If any ground is left unaddressed, a Miscellaneous Application can be a powerful remedy to seek recall of the order rather than merely correction.

Conclusion

The Pune Bench’s ruling in M/s. Sai Wardha Power Generation Ltd. v. DCIT underscores the importance of comprehensive adjudication in appellate proceedings. By recognizing non-consideration of grounds as a mistake apparent from the record, the Tribunal has strengthened procedural fairness and provided clarity on the scope of Section 254(2). This decision will undoubtedly serve as a guiding precedent in future litigation, ensuring that no argument raised by an assessee goes unheard.